| Parameter | Data |

|---|---|

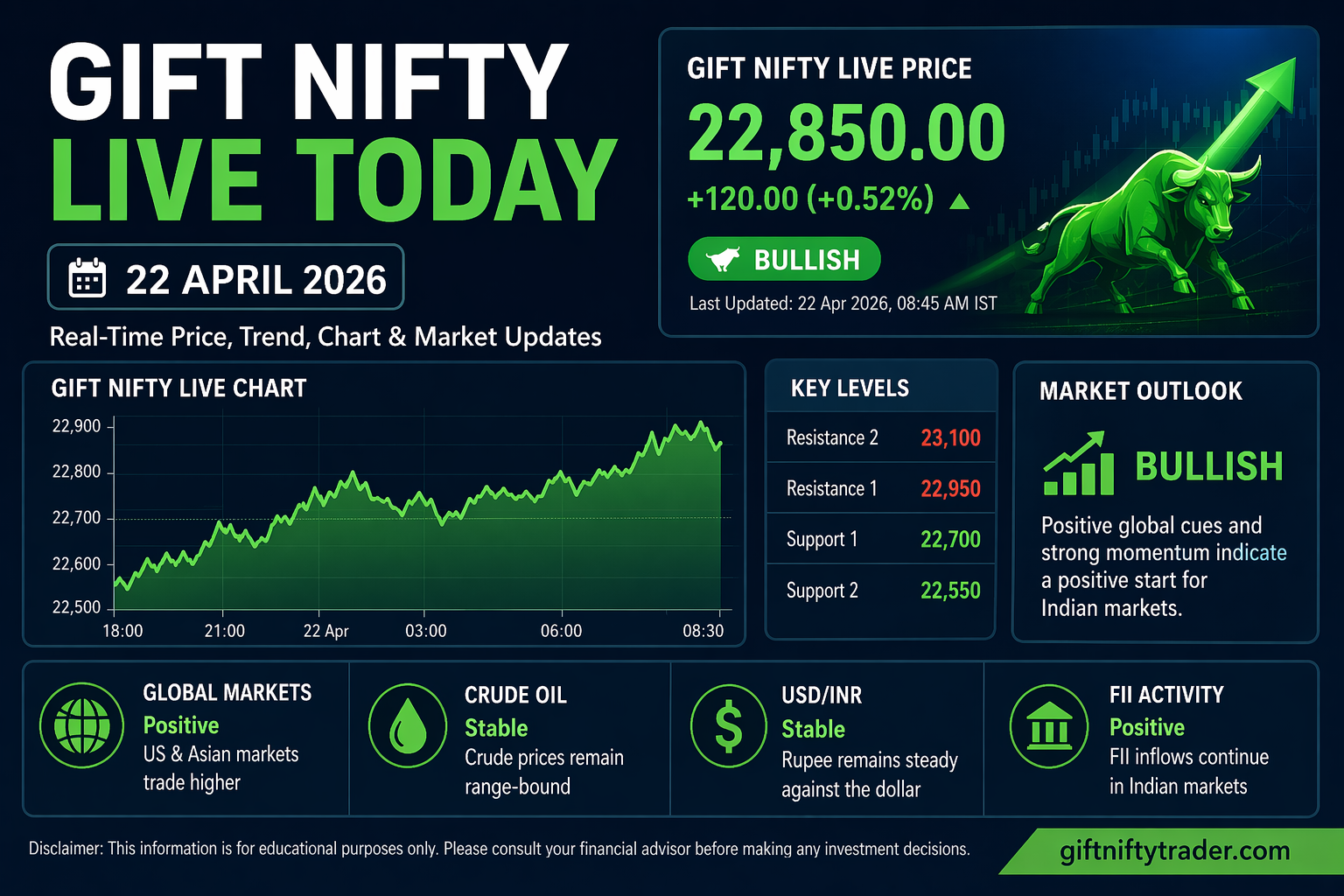

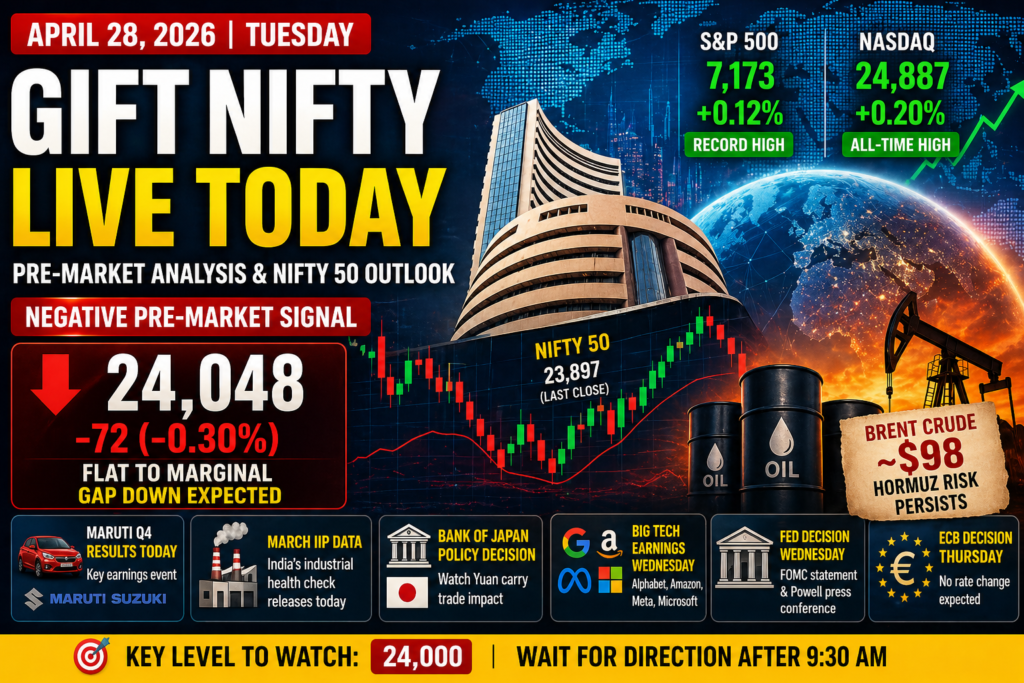

| 📡 Gift Nifty Live Price | ~24,048 |

| 📊 Change | –72 points (–0.30%) |

| 🚨 Signal | 🔴 Negative — Flat to Marginal Gap Down Expected |

| 🔺 Session High | 24,146 |

| 🔻 Session Low | 23,984 |

| 📈 Nifty 50 Last Close (Apr 25) | ~23,897 |

| 🏦 Bank Nifty Last Close | ~56,090 zone |

| 🛢️ Brent Crude | ~$98 — Off $101 peak, Hormuz risk persists |

| 🌍 S&P 500 (Monday close) | 7,173 — Record High (+0.12%) |

| 🌍 Nasdaq Composite (Monday) | 24,887 — All-Time High (+0.20%) |

| 📊 India VIX | Elevated — Options market pricing caution |

| 🚀 Big Events Today | Maruti Q4 Results · March IIP Data · BOJ Policy Decision |

| 🚀 Monster Event Wednesday | Alphabet · Amazon · Meta · Microsoft — Q1 Earnings |

Good morning, traders. Welcome to your gift nifty live today briefing for Tuesday, April 28, 2026. If you are checking your phone, scanning headlines, and wondering whether to go long or flat this morning — stop, and read this first. Because today is one of those sessions where the surface reading of the pre-market signal and the full picture underneath it are telling two very different stories. Walking into today’s market without understanding both could cost you more than just a bad trade.

Let us begin with what the numbers say. The gift nifty live reading at 8:00 AM IST is approximately 24,048 — down around 72 points from Monday’s reference levels. The sgx nifty today equivalent confirms the same direction. The signal heading into the 9:15 AM NSE open is cautious and marginally negative. A flat to small gap-down is what the pre-market is telling you to prepare for.

But here is the real story inside that number.

Monday’s session in the United States was genuinely constructive. The S&P 500 extended its winning run and closed at yet another record high. The Nasdaq Composite reached a new all-time high as well, driven by continued optimism around artificial intelligence infrastructure spending and the imminent wave of Big Tech earnings starting Wednesday. The US markets are in a remarkable place right now — April is shaping up as one of Wall Street’s strongest months in several years, and investor sentiment in America is running warm.

Yet Gift Nifty is negative. Indian futures are pointing down while American indices are printing all-time highs. Why?

Three reasons — and understanding all three is essential before you place a single order today.

First: crude oil. Brent crude is still hovering near $98 per barrel after briefly kissing $101 last week. Every single day that oil stays above $90 is a slow bleed for the Indian macroeconomic picture — wider current account deficit, rupee pressure, margin compression across dozens of industries. The Strait of Hormuz situation has not resolved. Peace talks between the United States and Iran have stalled again. Until the energy supply chain through the Gulf normalises, crude will remain a ceiling on Indian equity sentiment.

Second: FII selling. Foreign Portfolio Investors have been offloading Indian equities relentlessly through April 2026 — net selling of over Rs 44,000 crore for the month. On Friday alone, FIIs sold Rs 8,827 crore worth of Indian stocks. The primary reason is not India-specific weakness — it is the global rate environment. With US Treasury yields elevated and the dollar firm, global capital is finding dollar-denominated assets relatively more attractive, pulling money out of emerging markets including India.

Third: Monday was not a clean day for India. While Asia broadly was mixed — some markets up, some flat — Indian sentiment carried the residual damage from last week’s brutal IT sector crash (–5.29% in a single session) and three consecutive sessions of index losses into the weekend. The market is technically fragile at current levels, and it needs a fresh positive catalyst — not just Wall Street records — to decisively recover.

That is the full picture behind the Gift Nifty number this Tuesday morning.

📌 Track Gift Nifty live price, updated every minute: → Gift Nifty Live Chart & Signal — GiftNiftyTrader.com

Last Session Recap — What Monday Delivered & Why It Shapes Tuesday

Before we map out today’s strategy, let us settle what Monday gave us — because yesterday’s price action is the foundation of today’s context.

Monday, April 27 was a session built on hope but constrained by reality. GIFT Nifty had signalled a negative start, and the Indian market obliged — opening in negative territory with the shadow of crude oil and geopolitical uncertainty hanging over proceedings. The Nifty 50 and Sensex spent most of Monday’s session trading cautiously, with buyers unwilling to commit fresh capital in size given the dense event calendar ahead.

Asian markets told a split story. Japan’s Nikkei and South Korea’s Kospi showed strength — both recording notable gains during Monday’s Asian session, driven by optimism filtering in from Friday’s Wall Street surge and a chip sector rally in the United States that rippled across semiconductor-heavy Asian indices. But India did not fully participate in that Asian positivity. The rupee remained under pressure. The oil overhang did not ease. And FII flows — provisional data from NSE — once again showed net selling, adding to the cumulative April pressure.

The one consistent theme holding the Indian market from a sharper breakdown has been Domestic Institutional Investors. DIIs continued to buy on dips Monday, as they have done throughout April — deploying systematic investment plan money and active fund allocation into quality large-caps at what many fund managers consider a reasonable valuation entry point. DII support is real and structural. But it is not unlimited, and it has not been enough to push the Nifty decisively above the 24,000 psychological barrier on a sustained closing basis.

That 24,000 level — lost on a closing basis last week — is the market’s key psychological battleground. Monday did not reclaim it cleanly. Tuesday gets another shot.

Closing the session near 23,897, the Nifty 50 enters Tuesday with three consecutive weekly losses as the backdrop and a loaded data and event calendar ahead. The path of least resistance technically remains downward — but the fundamental setup for a reversal is building, especially if global Big Tech earnings starting Wednesday deliver the positive surprise the market is pricing in.

🌍 Global Market Cues — What the World Did While India Was Closed

| Market / Indicator | Direction | Signal for India |

|---|---|---|

| S&P 500 (Monday close) | 7,173.91 · +0.12% · Record Close | ✅ Positive sentiment |

| Nasdaq Composite (Monday) | 24,887.10 · +0.20% · All-Time High | ✅ Positive — AI/Tech bid |

| Dow Jones Industrial Average | 49,167.79 · –0.13% | ⚠️ Mixed — old economy softness |

| S&P 500 Futures (Pre-open) | ~7,203 · Strong Buy signal (technical) | ✅ US continuing higher |

| Japan Nikkei 225 | BOJ meeting today — market cautious | ⚠️ Wait-and-watch |

| Brent Crude Oil | ~$98 — Hormuz risk unresolved | 🔴 Negative for India |

| WTI Crude | ~$89 — Eased from intraday peak | 🔴 Still elevated |

| US Dollar Index | Firm — rupee under pressure | 🔴 FII flow headwind |

| Gold | Elevated — geopolitical safe-haven bid | ⚠️ Risk-off undercurrent |

| US 10Y Treasury Yield | Elevated — above 4.5% zone | 🔴 FII selling pressure on EM |

The Big Overnight Picture

Wall Street on Monday was a tale of quiet but steady record-making. The S&P 500 ticked to a new all-time closing high — a 0.12% gain that sounds modest but carries enormous psychological significance after the geopolitical turbulence of recent weeks. The Nasdaq Composite did the same, adding 0.20% to plant itself at a new all-time peak. The Dow, more sensitive to rate and cyclical concerns, dipped fractionally — the only blemish on an otherwise constructive US session.

The driving force behind US markets right now is unmistakably the AI narrative — and its validation through earnings. The semiconductor sector’s extraordinary results last week set the stage, and this week the software, cloud, and digital advertising giants step into the spotlight. The market is not just rallying on hope; it is beginning to see actual earnings evidence that the hundreds of billions of dollars being poured into AI infrastructure are generating real revenue acceleration.

For Indian markets, this US positivity is a good backdrop — but it is not sufficient on its own to neutralise the domestic headwinds of elevated crude and FII selling. What it does do is prevent a panic-driven collapse. India is stuck in a holding pattern until Wednesday’s Big Tech results provide the next definitive directional catalyst.

🎯 Gift Nifty Live Signal — Tuesday Morning Verdict

At 8:00 AM IST, the gift nifty live price is around 24,048 — down approximately 72 points from prior reference levels. Traders checking gift nifty live chart tradingview, gift nifty live groww, gift nifty live moneycontrol, and gift nifty live equitypandit will see consistent readings across platforms: a cautiously negative pre-market signal pointing toward a flat to marginal gap-down open for Nifty 50.

Gap context: Gift Nifty at ~24,048 versus Nifty 50’s Friday close of approximately 23,897 technically suggests a gap-UP of around 150 points on the face of it — but this reading requires nuance. Monday’s Indian session saw some pre-market buying; actual gap calculation depends on Monday’s closing data which may narrow the differential. The cleaner read is this: Gift Nifty’s overnight drift lower within its own session indicates sellers are not absent at these levels. The 24,000 resistance zone is doing its job.

Unlike last Monday’s marginal negative signal, today’s reading sits in a slightly better zone because Gift Nifty itself has been traversing the 23,984–24,146 intraday range — a tighter band that suggests neither aggressive sellers nor confident buyers. This is a market in genuine indecision, waiting for a catalyst. Wednesday’s Big Tech earnings will be that catalyst. Tuesday’s task — keep the floor intact.

Tuesday Pre-Market Verdict: 🔴 Flat to Marginally Negative | Expected Opening Zone: 23,900–24,100 | Bias: Cautious — Indecisive Until 9:30 AM | Key Level: 24,000 must close above to signal recovery

🏦 Bank Nifty & Sector Analysis — April 28, 2026

🏦 Banking — The Index’s Centre of Gravity

The Financial Services sector carries the heaviest weight in Nifty 50, and banking stocks’ behaviour at the open will define the entire session’s tone. The banking narrative heading into Tuesday is one of selective strength — private sector banks, particularly those that have already reported Q4 numbers showing strong net interest margins and improving asset quality, are in fundamentally better shape than the index’s recent performance suggests.

ICICI Bank reported solid Q4 numbers last week and provided a constructive template for what quality private banking looks like in the current environment: disciplined loan growth, contained slippages, and improving return ratios. HDFC Bank and Kotak Mahindra Bank will be the next critical data points. Axis Bank’s numbers will matter for reading mid-cap private banking health.

The risk for banking today comes from two directions. One: if crude stays elevated and the rupee weakens further, concerns about RBI’s rate path could dampen the rate-sensitive NIM (Net Interest Margin) story for banks. Two: if FII selling intensifies intraday, banking stocks — being the most liquid, FII-favoured names — absorb the heaviest supply pressure.

Watch Bank Nifty’s behaviour between 9:15 and 9:45 AM. Its first 30-minute range will tell you whether the day has buyers or sellers in charge.Bank Nifty Key Levels — April 28, 2026:

- Resistance: 56,400 → 56,700 → 57,000

- Support: 55,700 → 55,300 → 55,000 (critical psychological floor)

- Trend: Consolidating — needs a close above 56,500 to signal fresh bullish momentum

💻 IT Sector — Between a Rock and a Catalyst

The Nifty IT index is in a delicate position heading into Tuesday. Last week’s brutal 5.29% single-session crash following a major earnings disappointment from an IT heavyweight has left technical damage that will take multiple sessions to repair. However, the forward-looking story for Indian IT is not dead — it is simply suspended until Wednesday’s global Big Tech earnings provide fresh evidence.

Here is the logical chain that every IT investor should be tracking: if Alphabet, Amazon, Meta, and Microsoft collectively report strong AI infrastructure spending, cloud revenue acceleration, and enterprise software demand growth on Wednesday evening, Indian IT service companies benefit directly — they are the implementation and services layer for these global technology spends. A strong Wednesday from global Big Tech would likely trigger a relief rally in beaten-down Indian IT stocks on Thursday.

But Tuesday, the day before that potential catalyst, is not the time to build aggressive IT longs. The sector is technically broken. Institutional distribution is still happening. Waiting 24 hours for Wednesday’s earnings outcome before re-entering IT is the disciplined move. If the results disappoint, you will have saved yourself significant capital. If they impress, a Friday rally in IT names will still offer excellent risk-reward entries.

⛽ Oil Marketing Companies — Margin Squeeze Continues

HPCL, BPCL, and Indian Oil remain in the most difficult operating environment in recent memory. With Brent crude near $98, the refining margin compression is real and the political calendar — no state government wants higher petrol and diesel prices — means retail price relief is not imminent. These stocks will underperform until oil normalises below $85 on a sustained basis. Avoid fresh directional positions in OMCs this week.

✈️ Aviation — Turbulence Ahead of Results

Aviation stocks are the most directly exposed sector to jet fuel pricing, and every rupee move in crude compounds a rupee weakness environment. IndiGo’s Q4 results, when they arrive, will be closely watched for management commentary on fuel hedging, load factors, and passenger yield. Until then, treat aviation as a sector to avoid rather than trade in either direction. The options market is likely pricing elevated implied volatility in these names through the week.

🚗 Auto — Maruti Suzuki Takes the Spotlight Today

Maruti Suzuki reports its Q4 2026 results today, and this is the most important domestic earnings event of Tuesday’s session. Maruti is not just an auto stock — it is a barometer of mass-market and semi-urban consumer sentiment in India, rural income health, and fuel-price sensitivity at the household level. A strong Q4 result with volume growth and healthy margins would be a genuine positive for broader market sentiment, signalling that domestic consumption has held up despite macro headwinds. A disappointment — particularly any commentary about demand slowdown or margin pressure from input costs — would accelerate selling in the consumption space. Time the Maruti result carefully; it lands before market open.

💊 Pharma — Defensive Fortress in a Stormy Week

Pharma continues to be the sector that money rotates into when everything else looks uncertain. Sun Pharma, Dr. Reddy’s Laboratories, Cipla, and Divis Laboratories have all shown relative strength during April’s broader market weakness. The sector benefits from a weaker rupee (a significant portion of revenues are dollar-denominated exports), limited sensitivity to crude oil, and defensive earnings characteristics. If you need to be long something this Tuesday, quality pharma at a technically well-defined support level is the risk-adjusted answer.

📊 Nifty 50 Key Support & Resistance Levels — April 28, 2026

🟢 Support Levels

| Level | Zone | Note |

|---|---|---|

| 24,000 – 23,950 | Immediate Support | Psychologically critical — must hold on closing basis |

| 23,850 – 23,800 | 50-Day EMA Zone | Medium-term trend defence; last week’s closing region |

| 23,700 | Critical Structural Floor | Breakdown below here opens 23,400–23,200 |

| 23,500 – 23,400 | Strong Demand Zone | Historically strong DII and LII accumulation zone |

| 23,200 | Deep Support / Last Resort | Medium-term bull case survival level |

🔴 Resistance Levels

| Level | Zone | Note |

|---|---|---|

| 24,100 – 24,150 | Immediate Resistance | Gift Nifty session high zone — first ceiling today |

| 24,250 – 24,300 | Key Resistance Band | Previous support converted to resistance after breakdown |

| 24,500 | 200-Day EMA Region | Reclaiming this level = medium-term trend reversal signal |

| 24,600 – 24,700 | Strong Overhead Supply | FII selling likely to intensify in this zone |

📐 Technical Reading — April 28, 2026

Nifty 50 is trading below its 24,000 psychological level and below its 200-day EMA — both are technically significant. The index has been forming a pattern of lower highs and lower lows since mid-April, a classic definition of a short-term downtrend. Relative Strength Index on the daily chart is neutral to mildly oversold, meaning the selling momentum is not extreme but the buying conviction is also not present.

The one saving grace in the technical picture is volume. Recent selling sessions have not been accompanied by panicking, capitalisation-destroying volume. This suggests institutional liquidation rather than retail panic — and institutional selling, by its nature, tends to be more measured and methodical. When the fundamental backdrop shifts — crude normalises, FII selling abates, earnings clarity arrives — institutional money can reverse course relatively quickly.

The week’s most important technical level: 23,700. Three consecutive closes below 23,700 would be a technical amber alert for medium-term bulls. A weekly close above 24,200 this Friday would begin repairing the damage. Tuesday’s job is simply to hold the current floor and not create fresh technical damage going into Wednesday’s massive global catalyst.

💰 FII & DII Activity — April 2026 Picture

| Investor Type | MTD April 2026 (Estimated) | Friday Apr 25 (Single Day) | Direction |

|---|---|---|---|

| FII / FPI (Foreign Institutions) | ~–₹44,281 Crore Net Sold | –₹8,827 Crore | 🔴 Heavy Net Sellers |

| DII (Domestic Institutions) | ~+₹33,000+ Crore Net Bought | +₹4,700 Crore | ✅ Consistent Net Buyers |

| Net Position | ~–₹11,000 Crore net negative | –₹4,127 Crore | 🔴 Net sellers dominate |

April 2026 is the heaviest FII selling month of this calendar year for Indian equities — and the data is stark. Foreign Portfolio Investors have collectively offloaded nearly Rs 44,281 crore worth of Indian shares this month, driven primarily by the elevated crude oil environment (which worsens India’s macro fundamentals), rising US Treasury yields (which make dollar assets more attractive relative to emerging market risk), and residual geopolitical uncertainty from the Middle East conflict.

Domestic institutions have been the market’s spine throughout this selloff — buying into every dip, deploying systematic investment plan money from retail investors, and absorbing FII supply with discipline. Without DII support, the Nifty 50 could easily have been 1,000–1,500 points lower from current levels. The structural strength of India’s domestic investment ecosystem — with monthly SIP inflows consistently robust — is the single most important reason this market has not experienced a deeper correction despite such heavy FII selling.

What to watch today: NSE India publishes provisional FII and DII data from approximately 3:30 PM onwards. If today’s FII net selling comes in below Rs 1,500 crore, it signals moderation and markets will react positively. If net FII selling exceeds Rs 4,000 crore today, tomorrow’s pre-open — and Wednesday’s Gift Nifty signal — will face fresh pressure regardless of what happens in the US market Tuesday night.

📈 March 2026 IIP Data — India’s Industrial Health Check Today

One of Tuesday’s most important domestic data points — March 2026 Index of Industrial Production (IIP) — is scheduled for release today. IIP is the most comprehensive monthly indicator of industrial output momentum across manufacturing, mining, and electricity generation in India, and this particular reading carries extra significance for a market that has been questioning whether India’s real economy is absorbing the external shocks as well as equity bulls have been hoping.

A reading above 4.5% year-on-year would be broadly positive — signalling that industrial activity held up through March despite the early rumblings of geopolitical disruption. A reading below 3% would add to macro concerns and potentially accelerate selling in industrials, infrastructure, and capital goods stocks.

Watch the manufacturing sub-index particularly closely. Consumer durables and capital goods output within the IIP will tell you whether domestic demand and private investment intentions remained healthy in Q4 FY2026 — the answer to that question is critical for earnings guidance expectations across multiple Nifty sectors.

🚀 This Week’s Defining Moment — Global Big Tech Earnings Wednesday

Tuesday is important. But Wednesday evening after US market hours is where this week’s story truly gets written.

Four of the most consequential technology companies in the history of global capitalism report their first-quarter 2026 earnings results on Wednesday — a single-day earnings event of unprecedented scale that will simultaneously answer the most important questions facing global equity markets right now. Are the hundreds of billions of dollars being spent on AI infrastructure translating into revenue? Is enterprise technology demand growing or stalling? Are cloud computing revenues accelerating or hitting a saturation point? What is the health of digital advertising spending globally?

For Indian traders, Wednesday night’s global Big Tech results matter across multiple dimensions.

The most direct impact is on Indian IT stocks — a sector that has just suffered a brutal single-session crash of over 5% and is sitting at technically damaged levels. If the global technology earnings on Wednesday show strong AI-related enterprise spending, Indian IT service companies that implement, integrate, and support these technology platforms across global enterprises will see immediate re-rating. The beaten-down IT names could reverse sharply and quickly on Thursday’s Indian open. Conversely, if the results disappoint — if cloud growth is slower than expected or AI capex is questioned — Indian IT faces another leg down.

The broader market impact is through the FII flow channel. Strong global Big Tech earnings would improve global risk sentiment, potentially moderating the pace of FII outflows from emerging markets like India. Even a partial improvement in FII selling — say, from Rs 5,000 crore daily to Rs 1,000–2,000 crore — would give DII support enough room to stabilise, and potentially recover, the Nifty 50.

Mark this clearly on your calendar: Wednesday evening, after US market close. The Gift Nifty reading at 6:30 AM on Thursday morning will be entirely shaped by what those four companies deliver.

🏛️ Triple Central Bank Week — BOJ Today, Fed Wednesday, ECB Thursday

This week brings a sequence of central bank decisions that adds another layer of volatility to an already packed calendar. The Bank of Japan decides today (Tuesday), the US Federal Reserve on Wednesday, and the European Central Bank on Thursday. No rate change is expected from any of the three. But in markets running at record highs with elevated geopolitical uncertainty, central bank language — even a single phrase in a press conference — can move markets decisively.

The Bank of Japan’s decision today is directly relevant for Indian markets through the currency channel. Any BOJ signal about tightening policy or Yen management could trigger unwinding of the Yen carry trade — where global investors borrow cheap Yen and invest in higher-yielding assets including Indian equities and bonds. A Yen carry unwind would increase selling pressure across emerging markets including India, even if the RBI takes no action itself.

The Federal Reserve’s Wednesday decision and Chair Powell’s subsequent press conference is arguably the most market-moving event of the week for India — more so even than the Big Tech earnings. If the Fed signals that rates will stay elevated for longer than the market expects — particularly citing oil-driven inflation risks — US yields will rise, the dollar will strengthen, and FII selling into India will accelerate. If the Fed strikes a more neutral-to-dovish tone, the relief for emerging markets could be substantial and swift.

Trade accordingly: Tuesday is pre-positioning day. Cash is not a dead position when the Fed and four of the world’s largest technology companies are speaking within 24 hours of each other.

📅 Key Events — Week of April 28, 2026

- 🕤 Today (Apr 28), 9:15 AM — NSE opens. Expected flat-to-marginal gap-down. Critical: does 24,000 hold on closing basis?

- 📊 Today — Maruti Suzuki Q4 Results — Most important domestic earnings event of the session. Released before market open

- 📊 Today — March 2026 IIP Data — Key industrial output indicator for FY26 final quarter

- 🏛️ Today — Bank of Japan Policy Decision — Watch for Yen carry trade implications

- 🛢️ All Day — Monitor Brent crude. Above $100 = renewed selling trigger; below $92 = market relief

- 📊 Today 3:30 PM+ — Provisional FII/DII data on NSE India. Most critical directional input for Wednesday’s Gift Nifty reading

- ⚡ Tuesday (Apr 28) Evening — US markets open. Last clean session before Big Tech results

- 🚨 Wednesday (Apr 29) After US Close — Alphabet · Amazon · Meta · Microsoft Q1 2026 Earnings — The week’s defining event for Indian IT and global risk sentiment

- 🏛️ Wednesday (Apr 29) — US Federal Reserve rate decision and Chair Powell press conference

- 🏛️ Thursday (Apr 30) — European Central Bank rate decision

- 🇮🇳 Friday (May 1) — Maharashtra Day — NSE/BSE Closed. Reaction to Wednesday’s global events compressed into Thursday’s session

- 💱 Friday (May 1) — India Forex Reserves data release

🧭 Tuesday Strategy — Practical Guidance for Indian Traders

The strategic framework for Tuesday, April 28, 2026 is built around one core principle: preserve capital and position for Wednesday’s catalyst, not today’s noise.

This is a week where the most important market-moving events — Big Tech earnings and the Fed — happen after Tuesday’s session closes. Every trade you make today carries overnight risk through that event window. That is not a reason to be paralysed; it is a reason to be selective and size-disciplined.Scenario 1 — Bull case (25% probability): Nifty opens flat, Maruti Q4 beats estimates and triggers consumption sector buying, IIP data comes in strong above 5%, and the market closes above 24,100. This sets up a constructive pre-Fed positioning session. In this scenario, quality private banks and defensive pharma are your longs. Target 24,250–24,300 intraday. Scenario 2 — Base case (50% probability): Nifty opens flat to slightly down, trades a narrow 23,900–24,100 range through the session, closes near 23,950–24,050. No strong directional move either way. Market is essentially in holding mode ahead of Wednesday. In this scenario, reduce position sizing, avoid leveraged F&O trades, and let the market come to your entry points rather than chasing. Intraday scalpers can trade the range; swing traders should stay on the sidelines. Scenario 3 — Bear case (25% probability): Crude spikes back above $100 on fresh Hormuz headlines, Maruti disappoints on margins, IIP misses estimates, and Nifty breaks below 23,800 on an intraday basis. FII selling accelerates. This is the scenario where cash is the trade. If 23,700 breaks on a closing basis today, the Wednesday catalyst needs to be extraordinary to prevent a slide toward 23,400–23,200.

The one rule for Tuesday: Do not take large overnight positional bets before the Federal Reserve and Big Tech earnings. The risk-reward of carrying heavy leverage through a Fed meeting and four major earnings reports simultaneously is asymmetric in the wrong direction. Take your profits on intraday winners before 3:15 PM. Let the big positions wait for Wednesday’s clarity.

Check the gift nifty live chart and sgx nifty today signal updated in real time throughout the morning at GiftNiftyTrader.com.

⚠️ Disclaimer

GiftNiftyTrader.com is not affiliated with NSE, NSE International Exchange (NSE IX), BSE, SEBI, RBI, GIFT City, IFSCA, or any government or regulatory authority. All content in this post — including Gift Nifty live price levels, pre-market signal, Nifty 50 support and resistance levels, Bank Nifty analysis, sector commentary, FII/DII estimates, IIP discussion, trading scenarios, and all market data — is published strictly for informational and educational purposes only.

Nothing in this post constitutes investment advice, a recommendation to buy or sell any security, a solicitation to invest, or financial planning guidance of any kind. All market data referenced — Gift Nifty levels, index closing prices, FII/DII flow estimates, crude oil prices, and global market data — is derived from publicly available market sources and may be estimated, delayed, or subject to revision. Please verify all data independently before acting on it.

Trading in equity markets, futures and options, and derivative instruments involves very significant financial risk and may result in partial or total loss of invested capital. Past performance of any index, stock, or market is not indicative of future results. You are solely responsible for all your investment and trading decisions. GiftNiftyTrader.com, its authors, editors, and operators expressly disclaim all liability for any direct, indirect, incidental, or consequential financial losses arising from reliance on any content published on this website. Consult a SEBI-registered investment adviser before making any investment or trading decision.

📌 Bookmark GiftNiftyTrader.com — published every trading day at 6:00 AM IST. Your complete morning briefing for gift nifty live price, sgx nifty today signal, Nifty 50 levels, Bank Nifty outlook, and pre-market analysis.

→ Gift Nifty Live Chart | → Gift Nifty Today | → All Daily Updates